Oil at Three-Week High as US-Iran Peace Talks Stall

Good morning, and welcome to our continuous coverage of business, financial markets, and the global economy.

The new week begins with oil prices rising once again, as stalled US-Iran peace negotiations threaten to prolong disruptions to crude supplies from the Middle East.

Brent crude surged approximately 2% this morning, reaching $107.97 per barrel, marking its highest level since the ceasefire agreement on April 7.

Prices increased following former President Donald Trump’s cancellation of plans to send US envoys Steve Witkoff and Jared Kushner to Pakistan for ceasefire talks on Saturday, citing that “too much time” had been “wasted on travelling.”

“If they want to talk, they can come to us, or they can call us. You know, there is a telephone. We have nice, secure lines.”

However, there are indications of potential progress. Axios reports that Tehran has presented the US with a new proposal aimed at reopening the Strait of Hormuz and ending the conflict, with nuclear negotiations deferred to a later date.

Geopolitical developments will continue to influence markets as the week unfolds, coinciding with several major central banks scheduled to announce interest rate decisions.

Mohit Kumar, economist at Jefferies, commented:

“Talks have stalled between US and Iran as Iran has stated that it will not negotiate till the US blockade remains in place, while US has stated that it doesn’t know who it is negotiating with.

Our base case remains that we are moving towards a deal but tail risk of short term escalation remains. It is not in the interest of either parties to escalate further. The latest Iran proposal shows the wiliness of Iran to negotiate, while Trump already wants a deal. Hence, we believe that we will eventually move towards a deal, but with some speed bumps along the way.”

The Agenda

11am BST: CBI distributive trades survey of UK retail

3.30pm BST: Dallas Fed manufacturing index survey

Adidas Shares Rise After London Marathon Success

Shares of athletic apparel and footwear company Adidas increased by nearly 1.75% in early trading following outstanding performances by three of its sponsored athletes at the London Marathon yesterday.

Sabastian Sawe and Yomif Kejelcha both broke the two-hour barrier in the men’s marathon, while Tigist Assefa set a women-only world record in the women’s race.

All athletes wore Adidas’s Adizero Adios Pro Evo 3 shoes, and the company anticipates a sales boost from runners aiming to improve their own times.

Patrick Nava, general manager at adidas Running, stated:

“The adidas family is incredibly proud of Sabastian and Tigist’s historic achievements, marking the fastest times humans have ever run in a marathon.

This is a testament to the years of hard work and dedication they have made, alongside our innovation team, who have built a supershoe which breaks new ground in the Adizero Adios Pro Evo 3.”

Adidas shares rose to €138.55, up €2.30 this morning.

Unicredit issued a note on the oil market this morning, warning:

“The Iran war has triggered one of the largest disruptions to physical oil supply in modern history. While de‑escalation could ease some geopolitical risk premiums, the damage to production, exports and logistics means markets are unlikely to quickly return to pre‑war conditions.”

Goldman Sachs Raises Oil Price Forecast Amid War Disruption

The ongoing deadlock in the Middle East conflict has led Goldman Sachs to increase its oil price forecast.

Goldman Sachs now projects Brent crude to trade around $90 per barrel in the final quarter of this year, up from a previous estimate of $80. US crude is forecasted to average $83 in October-December, up from $75 earlier.

Goldman attributes the revision to “lower Persian Gulf production,” informing clients:

“We now assume a normalization in Gulf exports by end-June (vs. mid-May prior) and a slower Gulf production recovery. The economic risks are larger than our crude base case alone suggests because of the net upside risks to oil prices, unusually high refined product prices, products shortages risks, and the unprecedented scale of the shock.”

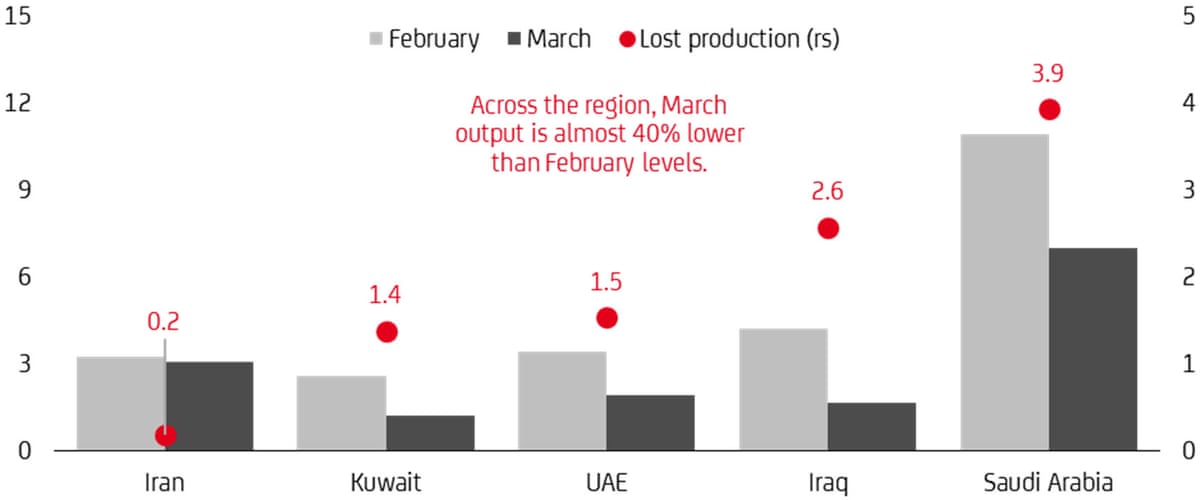

Goldman’s analysts estimate that 14.5 million barrels per day of Persian Gulf crude production have been lost, resulting in a record global oil inventory drawdown of 11-12 million barrels per day this month.

The surge in oil prices is expected to suppress demand, they explain:

“We assume that global oil demand falls on a year-over-year basis by 1.7mb/d in 2026Q2 and 0.1mb/d in 2026 given the jump in refined product prices. Because extreme inventory draws are not sustainable, even sharper demand losses could be required if the supply shock persists longer.”

Goldman also highlights that risks to its forecasts are skewed to the upside and outlines three possible scenarios:

- Adverse scenario: Brent 2026Q4 averages just over $100 assuming Gulf exports normalize by end-July.

- Severely adverse scenario: Brent 2026Q4 averages nearly $120 assuming Gulf exports normalize by end-July and a persistent 2.5mb/d reduction in Gulf capacity, equivalent to Hormuz flows not recovering above 70% until pipeline capacity expansion.

- Benign scenario: Brent 2026Q4 averages just under $80 assuming Gulf exports normalize by mid-June, no capacity reduction, and stronger US and core OPEC supply responses.

Sainsbury’s Shares Fall After Broker Downgrade

Following the US-Iran ceasefire announcement, supermarket chain J Sainsbury was the top decliner on the FTSE 100 in early trading after a broker downgrade.

Goldman Sachs downgraded Sainsbury’s rating from ‘buy’ to ‘sell’, lowering the share price target from 390p to 335p.

In response, Sainsbury’s shares declined 3.4% to 333p.

European Markets Open Slightly Higher Amid Middle East Uncertainty

European stock markets opened modestly higher as investors assessed the Middle East situation.

Axios’s report of Iran’s new proposal to the US to reopen the Strait of Hormuz may have contributed to a slightly improved market sentiment.

Germany’s Dax index rose 0.4% in early trading, France’s CAC 40 increased by 0.25%, while the UK’s FTSE 100 index remained flat.

This week promises to be busy for financial news.

Jim Reid, market strategist at Deutsche Bank, explained:

“Looking ahead, with central bank meetings for every G7 country this week — alongside 44% of the S&P 500 reporting by market capitalisation, including five of the Mag 7 — it is shaping up to be a blockbuster week, even before factoring in ongoing Iranian war newsflow.

The Bank of Japan meets tomorrow, followed by the Fed and the Bank of Canada on Wednesday. Thursday then brings decisions from the ECB and the Bank of England. All are expected to remain on hold, but the key question will be how each central bank’s reaction function is shaped by the conflict and the associated stagflation risks.”

European Gas Prices Rise Slightly

European gas prices increased modestly at the start of trading.

The month-ahead UK gas contract rose 0.8% to 112.8p per therm, up from 80p before the Iran conflict began but below the mid-March peak of 180p.

Continental European gas prices followed a similar trend; the next-month Dutch TTF Natural Gas Futures contract increased to €45.21 per megawatt hour.

Japan's Nikkei Hits Record High Above 60,000 Points on Peace Talk Hopes

Hopes for a breakthrough to end the Middle East conflict have propelled Japan’s stock market to a new record high.

The Nikkei 225 index closed up nearly 1.4%, reaching 60,537 points.

Stocks rallied after Axios reported that Iran submitted a new proposal to the US to end the war, easing concerns following President Trump’s cancellation of his envoys’ trip to Pakistan for peace talks.

Ipek Ozkardeskaya, senior analyst at Swissquote, commented:

“The mood is slightly better this morning than it was into the weekend, as Iran reportedly offered the US a proposal to reopen the strait of Hormuz — a move that could pave the way for the continuation of peace talks between the two parties.”

UK House Price Growth Forecast Halved Due to Middle East Conflict

UK estate agent Knight Frank has reduced its house price growth forecast for this year, citing economic shocks caused by the Iran conflict.

Knight Frank now anticipates UK house price growth of 1.5% in 2024, down from a 3% forecast made last September. Growth is expected to increase to 3% in 2027, down from a previous forecast of 4%.

Tom Bill, head of UK residential research at Knight Frank, explained:

“The Middle East conflict has pushed mortgage rates higher, dampened buyer sentiment and fuelled speculation about how the government will respond to the resulting economic shock.

This hat-trick of headwinds means we have revised down our near-term house price forecasts.”