Bank of England Holds Interest Rates at 3.75%

The Bank of England maintained its base interest rate at 3.75% during its first meeting of 2026, marking the lowest level since February 2023. This decision follows a reduction from 4% in December 2025. Analysts remain divided on the timing and frequency of any further rate cuts.

Interest rates directly impact mortgage payments, credit card charges, and savings returns for millions of UK residents.

What Are Interest Rates and Why Do They Change?

An interest rate represents the cost of borrowing money or the return earned on savings. The Bank of England's base rate is the rate it charges other banks and building societies to borrow funds, influencing the rates those institutions offer to their customers for mortgages and savings accounts.

The Bank adjusts this benchmark rate to maintain UK inflation at or near its 2% target. When inflation exceeds this target, the Bank typically raises rates to encourage reduced spending, thereby lowering demand for goods and services and limiting price increases.

Recent Trends in UK Interest Rates and Inflation

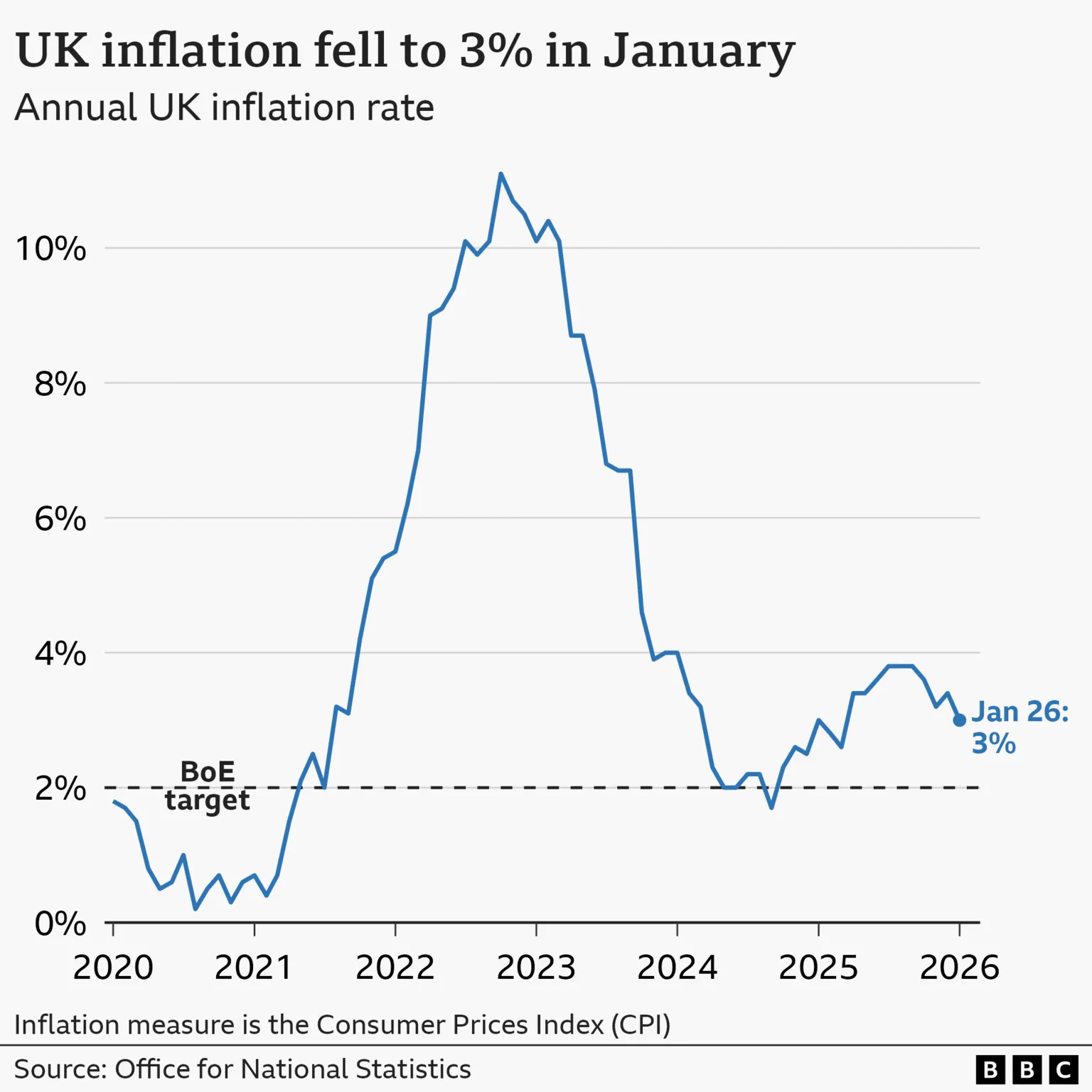

The Consumer Prices Index (CPI), the main measure of inflation, has declined significantly from a peak of 11.1% in October 2022. Inflation was recorded at 3% in the year to January 2026, down from 3.4% in December 2025. The Office for National Statistics (ONS) attributed this decrease to lower prices for fuel, food, and flights.

The Bank of England's base rate reached a recent high of 5.25% in 2023 and remained at that level until August 2024, when the Bank began reducing rates. Five successive cuts brought the rate down to 4%, followed by holds in September and November 2025, before the December cut and the January 2026 hold.

Prospects for Future Interest Rate Cuts

Most analysts anticipated the December 2025 rate cut; however, the nine-member Monetary Policy Committee (MPC) vote was narrowly split, with five members in favor. The January 2026 decision was similarly close, passing by a 5-4 vote.

"We now think that inflation will fall back to around 2% by the spring. That's good news. We need to make sure that inflation stays there. All going well, there should be scope for some further reduction in the Bank rate this year," said Bank of England Governor Andrew Bailey.

As inflation continues to decline, further rate reductions become more probable. Analysts generally forecast one or two cuts during 2026, with some traders expecting the first cut at the Bank's next meeting on 19 March 2026. The likelihood of a March cut increased after data showed a slowdown in wage growth.

Impact of Interest Rate Changes on Mortgages, Loans, and Savings

According to the government's English Housing Survey, just under one-third of households have a mortgage. Approximately 500,000 homeowners have tracker mortgages linked directly to the Bank of England's base rate, so any rate cut reduces their monthly repayments. Another 500,000 homeowners on standard variable rates (SVR) depend on lenders to pass on any Bank rate cuts.

The majority of mortgage holders, however, have fixed-rate deals. These customers' monthly payments are not immediately affected by changes in the base rate, though future mortgage deals will be influenced.

As of 18 February 2026, the average two-year fixed residential mortgage rate was 4.85%, and the five-year fixed rate was 4.97%, according to Moneyfacts. The average two-year tracker mortgage rate was 4.44%.

On average, about 800,000 fixed-rate mortgages with interest rates at or below 3% are expected to expire annually through 2027. Borrowers coming off these deals are likely to face significantly higher borrowing costs.

Bank of England interest rates also affect credit card, bank loan, and car loan interest rates. Lenders may reduce their rates following Bank cuts, but such changes tend to occur gradually.

The base rate also influences savers’ returns. A falling base rate typically leads to lower interest rates on savings accounts offered by banks and building societies. As of 18 February 2026, the average rate for an easy access savings account was 2.42%, according to Moneyfacts. Further rate cuts could particularly impact individuals relying on savings interest to supplement their income.

Interest Rate Trends in Other Countries

In recent years, the UK has maintained one of the highest interest rates among the G7 advanced economies. In June 2024, the European Central Bank (ECB) began cutting its main interest rate for the eurozone from an all-time high of 4%. At its June 2025 meeting, the ECB reduced rates by 0.25 percentage points to 2%, where they have remained since.

The US Federal Reserve has cut interest rates three times since September 2025, bringing them to a current range of 3.5% to 3.75%, the lowest level since 2022. The Fed held rates steady at its January 2026 meeting.

Former President Donald Trump had criticized the Fed for not cutting rates earlier and has nominated Kevin Warsh to lead the Federal Reserve when current Chairman Jerome Powell’s term ends in May 2026.