Introduction: UK house prices rise again in March

Good morning, and welcome to our continuous coverage of business, financial markets, and the global economy.

Nationwide, the building society, has reported that UK house prices increased by 0.9% in March compared to the previous month, and by 2.2% on an annual basis.

Robert Gardner, chief economist at Nationwide, states that the acceleration in growth indicates the housing market has regained momentum following a slow end to 2025. However, he warns this may be a temporary calm before potential disruption:

"The sharp rise in global energy prices in response to developments in the Middle East represents a significant shock to the global economy, clouding the outlook.

In the near term, UK economic growth is likely to be slower and inflation higher than previously expected, although ultimately the impact will depend on the duration of the shock as well as the policy response. The outlook for interest rates is particularly uncertain and dependent on whether the demand or supply side of the economy is more adversely affected."

In the first quarter of 2026, the average UK house price was £274,930, reflecting a 1.5% increase compared with the same period in 2025.

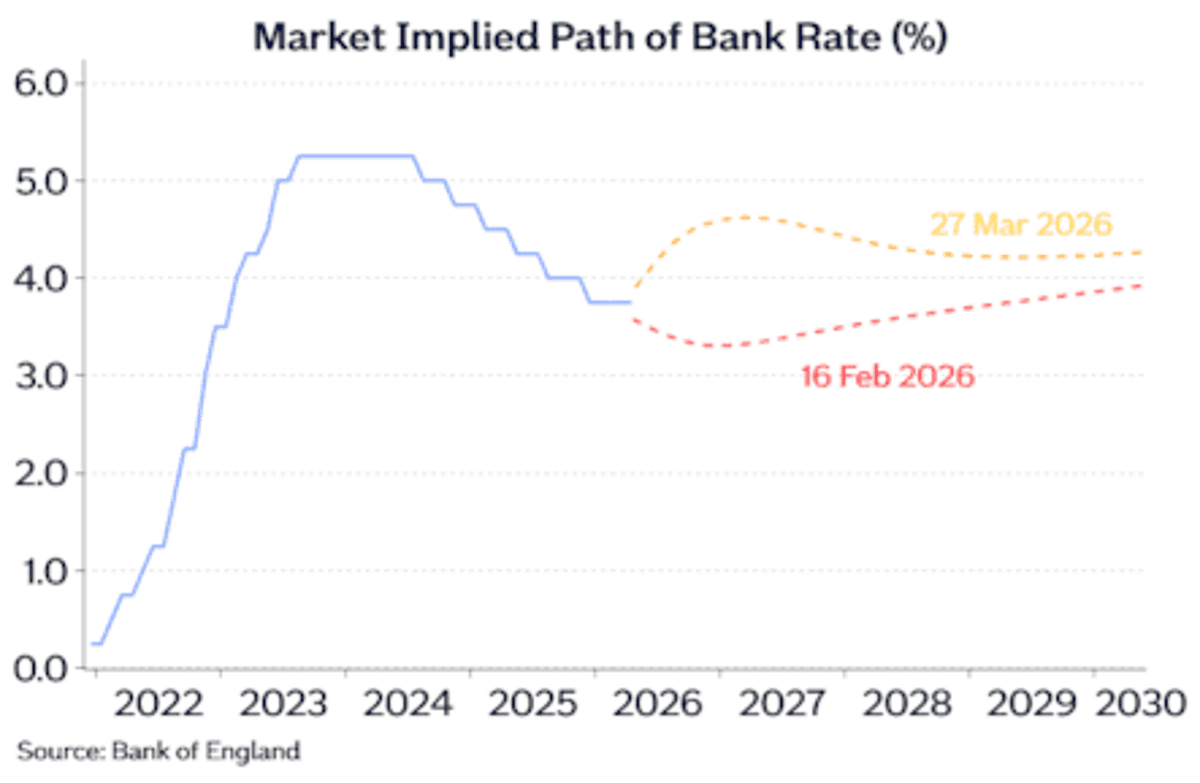

Gardner further notes that interest rates have shifted significantly since the onset of the Middle East conflict.

"Towards the end of March, three interest rate increases were priced in over the next twelve months, compared to two rate cuts being anticipated before the strikes on Iran. This shift has resulted in a sharp rise in longer term interest rates (swap rates) that underpin fixed rate mortgage pricing.

If sustained, this could reverse some of the improvement in housing affordability that has taken place in recent years. With consumer sentiment also likely to be dented by the uncertain outlook and the prospect of rising energy costs, housing market activity is likely to soften."

Tom Bill, head of UK residential research at Knight Frank, adds that mortgage offers, which last six months, mean the impact of higher borrowing costs will influence the market during spring and summer, potentially exerting downward pressure on prices and transaction volumes.

"The longer-term impact hinges on the intensity and length of the conflict. That said, one mitigating factor is the amount of equity in the system and the fact more homes are now owned outright than with a mortgage."

UK economic growth and revisions

Official statistics confirm that the UK economy showed minimal growth at the end of last year. The Office for National Statistics (ONS) reported that gross domestic product (GDP) grew by just 0.1% in the October to December quarter, matching growth in the previous quarter.

However, the ONS revised the annual growth rate for 2025 slightly upward from 1.3% to 1.4%.

Although the final quarter figures are modest, the Treasury issued a statement emphasizing confidence in the economic strategy:

"In an uncertain world we have the right economic plan. The decisions we have taken have put us in a better position to protect the country’s finances and family finances from global instability.

We were the fastest growing European economy in the G7 last year and now we’re going even further by using regional growth, AI and a closer relationship with the EU to get our economy growing."

Thomas Pugh, chief economist at RSM UK, offers a more cautious perspective:

"GDP growth for Q4 was unchanged at 0.1% quarter-on-quarter, suggesting that the economy entered the current crisis with very little momentum, even though growth in 2025 as a whole was revised up slightly.

Of course, backward looking is an understatement for Q4 data, the outlook for growth is now materially weaker for this year and 2027 as higher energy prices will squeeze real incomes and further weigh on an already weak employment market."

The agenda

- 8am BST: Kantar grocery inflation figures

- 10am BST: Eurozone CPI for March

UK grocery inflation at 4.3% in March

Consumers are facing rising costs, with food prices increasing as well, according to Worldpanel by Numerator. The research firm found UK grocery inflation at 4.3% in the four weeks ending March 22. Prices rose fastest in categories such as fresh unprocessed meat, skin care, and chocolate confectionery, while falling fastest in chilled butter and spreads, household paper, and sugar confectionery.

Fraser McKevitt, head of retail and consumer insight at Worldpanel by Numerator, comments on the impact of the Middle East conflict on prices:

"Financial anxiety among British consumers was already running high before the conflict began. And with grocery inflation likely to increase and fuel costs rising sharply, the conditions that make shoppers feel vulnerable are only intensifying."

Chocolate prices have risen notably, which is unwelcome news for those purchasing Easter eggs this week. The average cost of an Easter egg is now £3.27, a 9% increase compared with last year, according to Worldpanel.

Waitrose has experienced a strong month, with sales growing 5.6%, its fastest rate in five years. Its market share increased to 4.7%, up from 4.6% last year, marking its highest level in three years. Ocado was the fastest growing grocer again, with sales up 12.3%, although it holds only 2.2% of the market. Tesco remains the largest grocer with a 28% market share.

European markets and oil prices

European markets are subdued this morning. The UK’s FTSE 100 is nearly flat, rising slightly by 0.1%. France’s CAC 40 and Germany’s DAX are both up by 0.1%, while Italy’s FTSE MIB is down 0.3%.

Oil prices are edging higher, with Brent crude rising 0.6% to $113.43 a barrel.

Lenders’ shares rise after car finance scandal compensation scheme announced

Shares in lenders implicated in the car finance scandal are rising following the City regulator’s announcement of a compensation scheme last night.

Lloyds Banking Group shares rose 0.5% in early trading, Barclays increased by 0.7%, and specialist lender Close Brothers gained 0.8%. Santander, listed in Spain, also rose 0.8%.

The Financial Conduct Authority (FCA) revealed details of its redress programme for victims of the car finance scandal, where customers were overcharged due to commission payments between lenders and car dealers.

The FCA has narrowed the number of eligible loan agreements from 14 million to 12.1 million contracts, covering loans agreed between 2007 and 2024. This adjustment is expected to increase the payout per contract to £830, including interest.

Regional house price variations

Most UK regions experienced house price growth in the first quarter of 2026, except for the outer South East, which fell 0.7% year-on-year, and East Anglia, down 0.4%, according to Nationwide.

Northern Ireland continued to outperform, with house prices up 9.5% year-on-year in the first quarter—more than six times the UK average.

Robert Gardner adds:

"England saw a further slowing in annual house price growth to 0.9%, from 1.2% in Q4. Average prices in Northern England (comprising North, North West, Yorkshire & The Humber, East Midlands and West Midlands) were up 1.5% year on year, with the North West (which includes areas such as Cheshire, Lancashire & Greater Manchester) remaining the top performing region in England – with prices up 3.3% year on year.

By property type, detached properties performed the strongest, with prices up 2.4% year-on-year over the last 12 months. Terraced properties grew by 2.1%, with semi-detached slightly weaker at 1.5%. Flats fell by 0.5%."

Economic outlook and commentary

Jonathan Raymond, investment manager at Quilter Cheviot, notes that the UK economy "limped over the line" at the end of 2025, highlighting its vulnerability entering 2026.

"Growth was already fragile, and while there were tentative signs of life at the start of the year, the latest bout of geopolitical turmoil has quickly snuffed them out.

The UK has narrowly avoided the recession some feared would have arrived at some point in the past 18 months, but that should not be mistaken for strength. This is an economy stuck in stagnation.

After a promising start to the year, momentum faded as businesses paused investment in response to tax changes and households grew increasingly cautious about what comes next. Inflation, meanwhile, has remained stubbornly above target, keeping interest rates higher for longer and tightening the squeeze on activity."

Inflation remained steady, aligning with expectations but still well above the government’s 2% target.

"Looking ahead, higher energy prices are beginning to impact economic activity, raising the risk of softer demand as consumers and households retrench just as inflationary pressures re‑emerge.

…For the Bank of England, this presents an uncomfortable trade‑off. In normal circumstances, prolonged stagnation would argue for looser policy to support growth. But with inflation likely to rise again, the scope to cut rates is limited.

Markets may be overestimating how far policy needs to tighten with expectations for at least 2 quarter-point interest rate rises this year, but the Bank will have to remain agile in responding to this energy shock if it is to prevent today’s weakness from hardening into something more lasting."