Economic Impact of Iran Conflict Influences Bank of England's Interest Rate Decision

The ongoing war in Iran is anticipated to prompt the Bank of England to maintain current interest rates at its upcoming meeting. Prior to the conflict, analysts had forecasted a reduction in the Bank rate. However, market volatility and rising oil prices have largely eliminated the possibility of a rate cut.

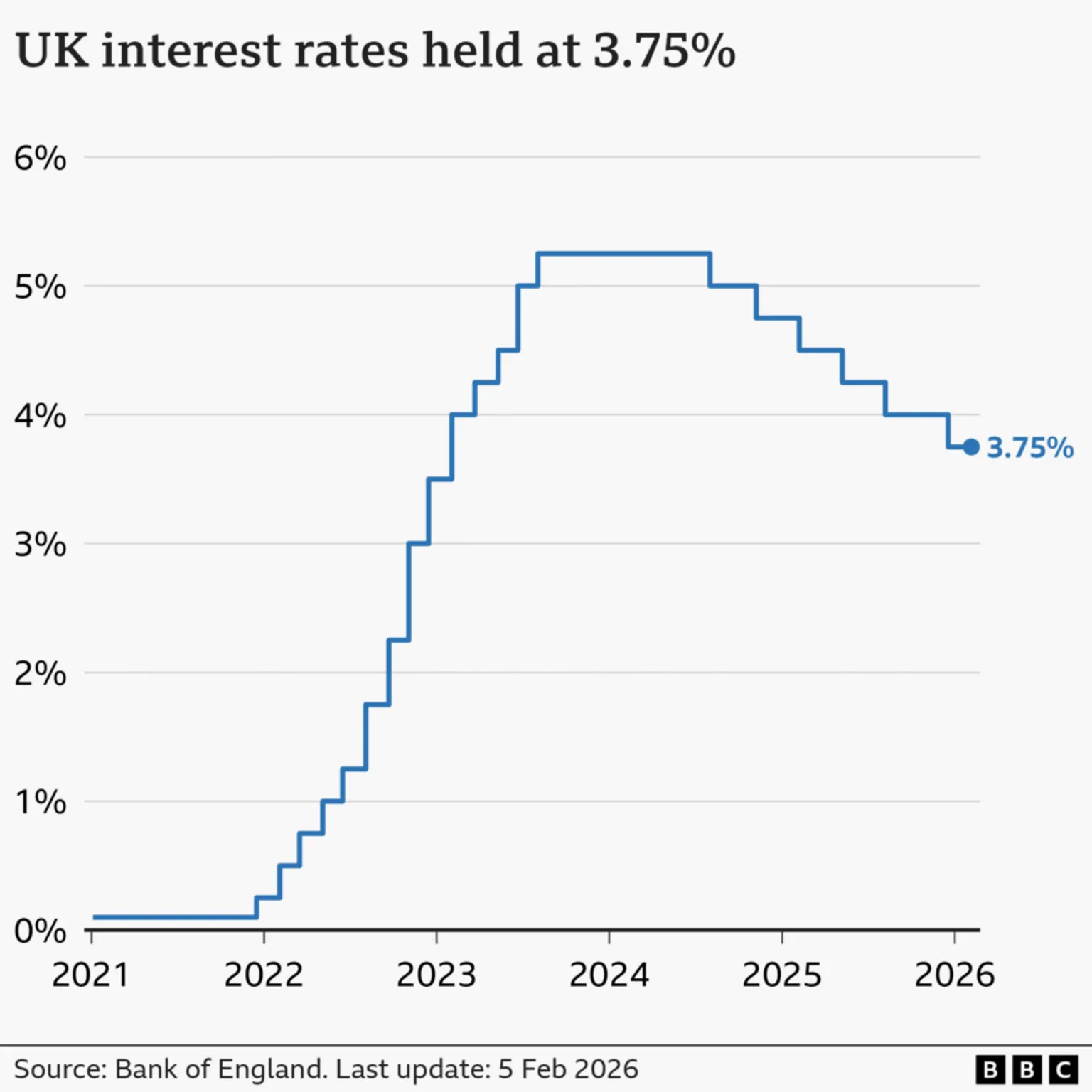

The Bank's Monetary Policy Committee (MPC) is expected to keep the benchmark interest rate, which affects borrowing costs for individuals and businesses, steady at 3.75%.

There is considerable uncertainty among commentators regarding the timing and frequency of any future interest rate reductions this year. Some analysts suggest that if the conflict persists and causes prolonged economic disruption, an interest rate increase could be considered.

The MPC's latest interest rate decision will be announced at 12:00 GMT.

Economists had anticipated a rate cut following the decline in inflation to 3% in January. The Bank rate was already at its lowest level since February 2023.

At the start of February, the Bank's rate-setters voted narrowly to hold the benchmark rate. At that time, Bank Governor Andrew Bailey told the BBC that a "some further reduction" in rates was likely later in the year.

However, the situation changed dramatically after the US-Israeli strikes on Iran, which have had significant economic repercussions in the UK and globally.

Oil prices have surged due to disruptions in critical trade routes, primarily the Strait of Hormuz.

This increase is expected to eventually impact domestic energy prices, leading to higher heating oil costs and increased petrol prices at the pumps.

Official forecasters predict that these factors will exert upward pressure on inflation, which had been expected to decline towards the 2% target.

Interest rates remain the primary tool the Bank uses to achieve its inflation target. Consequently, economists now expect the MPC to refrain from altering rates immediately, opting instead to assess the duration and severity of the price shock.

Mortgage Rates on the Rise

The Bank of England's base rate determines the interest rate it charges banks and building societies for borrowing money. This rate influences the interest rates these institutions offer to their customers for mortgages and savings.

Markets and lenders have priced in an interest rate hold, but the prevailing uncertainty has led to the withdrawal of some mortgage deals and an increase in rates on new fixed-rate deals.

According to the financial information service Moneyfacts, the average two-year fixed mortgage rate has risen from 4.83% at the start of March to 5.30% currently, marking its highest level since last February.

For those seeking a five-year fixed mortgage, the average rate has increased from 4.95% to 5.35% over the same period, reaching its highest point since August 2024.

Other borrowing costs, including rates on credit cards and personal loans, are also expected to be affected.

"This will be particularly challenging for lower income households, many of whom were hoping that falling rates would ease pressure on already stretched budgets," said Tamsin Powell, consumer finance commentator at Creditspring.

"Instead, they are now facing a prolonged period where the cost of credit remains high, while essentials like food, utilities and transport continue to take up a greater share of income. This leaves far less flexibility to absorb financial shocks or unexpected expenses."

A reduction in interest rates typically results in lower returns for savers. A rate hold should provide "some short respite," according to Rachel Springall of Moneyfacts.

"Over the past couple of weeks, there have been more savings rate increases than reductions, most notably on one-year fixed rates, but the true benefit rests in the margins, so average rates are not moving much," she said.

"The market needs stability and savers need to feel encouraged to build a nest egg."

Ms. Springall added that approximately 60% of UK savings accounts currently fail to offer returns that exceed the Bank rate of 3.75%.