Fuel prices for motorists

Drivers in the UK may have already observed an increase in fuel prices at petrol stations. By Sunday, average petrol prices rose by 4.68p to 137.51p per litre, while diesel prices increased by 8.59p to 150.97p per litre, according to the RAC motoring organisation.

Analysts estimate that every $10 rise in crude oil prices typically results in a 7p per litre increase at the pump. Since the onset of the US-Israeli war with Iran, crude oil prices have surged by more than $30, making petrol prices exceeding 140p per litre likely. If oil prices remain elevated, 150p per litre could soon be surpassed.

Although motoring organisations confirm that fuel supplies remain adequate, they advise motorists to reduce non-essential journeys and adopt fuel-efficient driving habits, such as avoiding harsh acceleration and braking, to conserve fuel.

Not all individuals own or regularly use a car, but rising petrol prices can indirectly lead to higher costs for goods and services. For instance, increased transport expenses for supermarkets may be reflected in food prices.

Cost and choice of mortgages

Prior to the conflict, there was anticipation of a gradual decline in interest rates for new fixed mortgages and lower variable rates in the UK. However, the opposite trend is now evident.

Major UK lenders have increased mortgage rates due to rising funding costs and expectations that the base borrowing rate will not decrease as previously forecasted. While mortgage rate increases for new or renewing two- or five-year deals have been moderate so far, further "painful" rises are anticipated, especially for borrowers seeking shorter-term deals.

As of 9 March, the average rate for a two-year mortgage deal rose to 4.87%, and the average five-year fixed rate increased to 4.98%, according to Moneyfacts. The last time both rates exceeded 5% was in August 2023.

Economic uncertainty has led some lenders to withdraw mortgage products, reducing consumer choice. Several lenders have removed their entire range of deals, planning to reprice them at higher levels.

"When lenders take the step of pulling deals rather than simply tweaking pricing, it often indicates that funding costs have moved too quickly for incremental changes to keep pace," said Adam French, head of consumer finance at Moneyfacts.

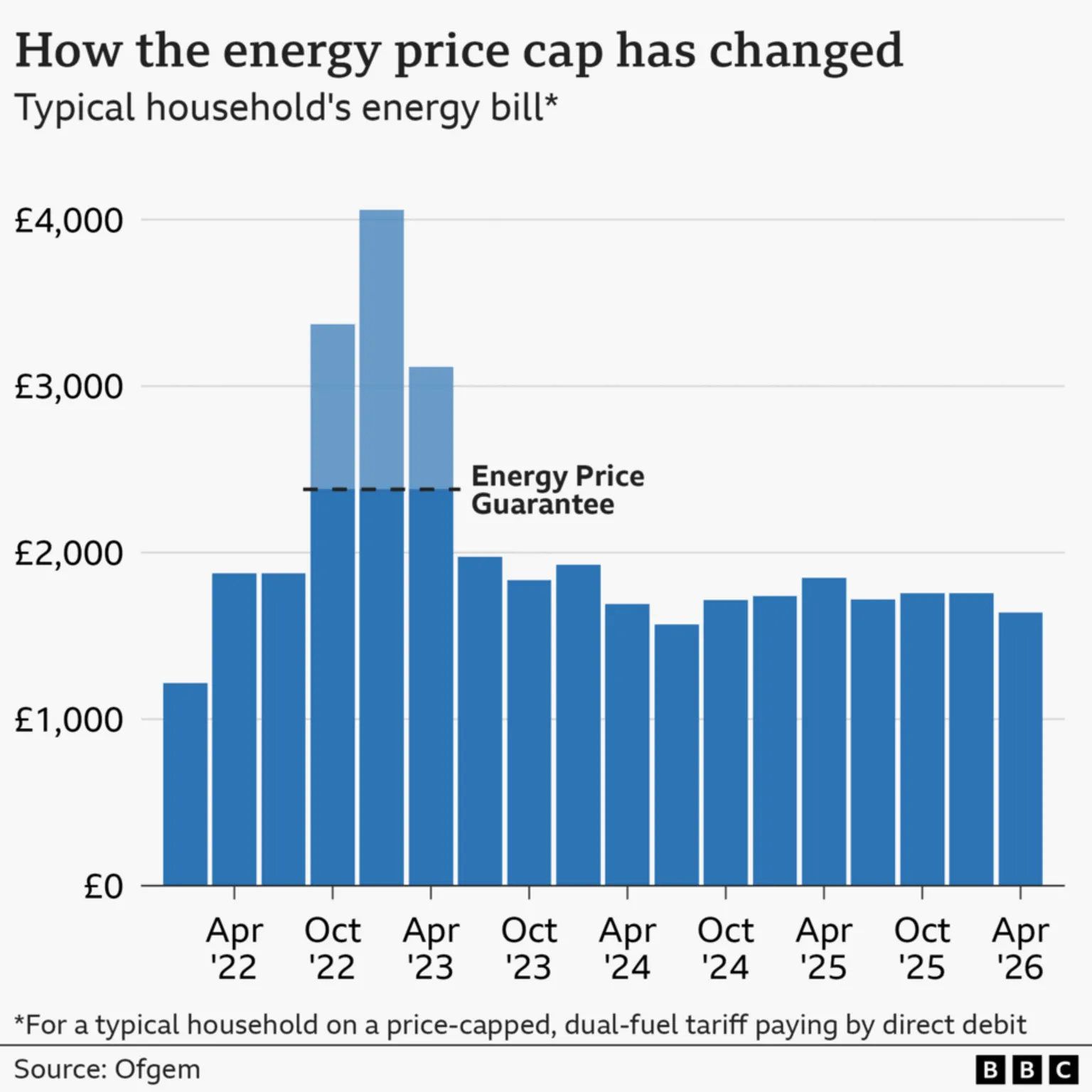

Energy bills and heating oil costs

Household gas and electricity bills in England, Wales, and Scotland benefit from a price cap set by energy regulator Ofgem, offering some protection. However, this cap is time-limited and does not cover all consumers.

The unit price for energy under variable deals governed by the cap is fixed until July, with prices expected to decrease in April. Nevertheless, wholesale energy market conditions between now and late May will influence household bills from summer onwards. Prolonged high wholesale costs could lead to significant increases in energy prices for millions.

The previous spike in energy prices, following the Covid-19 pandemic and Russia's invasion of Ukraine, prompted government intervention through the Energy Price Guarantee.

Consumers seeking to fix their energy unit price face challenges similar to mortgage seekers. Some energy tariff providers have withdrawn deals or set higher prices. Geopolitical uncertainty also reduces the availability of long-duration deals.

The most immediate effect of rising prices is on heating oil users, who typically store oil in tanks outside their homes. There is no price cap on heating oil, and campaigners report that prices have more than doubled since the conflict began. Panic buying has further strained supply.

"We may be heading into spring, but anyone running low on oil right now doesn't have the luxury of waiting for prices to fall," said Emma Simpson, chief executive of Rural Action Derbyshire.

Heating oil is commonly used in rural areas and Northern Ireland, where there have been calls for support for those struggling with payments.

Higher cost of living but with limits

At the beginning of March, UK inflation was forecast to be around the Bank of England's 2% target over the next five years, according to the Office for Budget Responsibility (OBR). The OBR projected that prices for a typical basket of goods would rise by 2.3% in 2024 and then 2% annually from 2027. However, these forecasts were made prior to the air strikes on Iran.

Analysts now consider these inflation estimates increasingly unlikely due to the volatile military and economic situation. Despite this, inflation is not expected to return to the peak of 11.1% recorded in the UK in October 2022. This is partly because the Ukraine conflict caused significant spikes in prices for basic foodstuffs like wheat and edible oil, a factor not present in the current situation.

Interest rates less likely to fall

The Bank of England aims to maintain inflation close to 2%, primarily using interest rate adjustments. Following the February rate-setting committee meeting, Governor Andrew Bailey indicated potential for rate cuts later in the year.

However, the likelihood of rate reductions has diminished. Analysts who previously expected borrowing costs to decrease in March have now ruled out this possibility. While borrowing may become more expensive than anticipated, savers could benefit from slightly higher returns.

Historically, periods of uncertainty have led to increased savings. However, rising living costs may reduce the purchasing power of saved funds and could negatively impact overall economic growth in the UK.

The price of fun

The broader financial implications depend heavily on the progression and global effects of the war. One immediate impact could be on holiday travel choices for spring and summer, which may become more limited and costly.

Jet fuel prices have risen sharply. Although airlines employ purchasing strategies to mitigate some of this impact, prolonged high aviation fuel costs are likely to result in increased airfares.