Ten years on, Brexit's economic impact is becoming clearer

Shortly after the UK exited the EU in 2020, Eskimo, a Bristol-based company, began marketing a novel high-fashion, energy-efficient electric radiator developed from local academic research. The firm intended to distribute these products across Europe via the Channel Tunnel. This product aligned well with Europe's environmental goals, and initial demand kept Eskimo's Birmingham factory busy.

Phil Ward, Eskimo's CEO, reports continued growth but notes the company’s potential was curtailed by what he terms "the Long Brexit effect." In 2020, 40% of Eskimo's exports were destined for the EU; by 2025, this figure had fallen to just 5%. Although the post-Brexit agreement negotiated by then-Prime Minister Boris Johnson in December 2020 ensured zero tariffs on EU exports, Ward highlights that non-tariff barriers such as increased paperwork and regulatory delays imposed costs and deterred customers.

Eskimo managed limited exports to French agents but ceased direct sales to European consumers and abandoned plans to expand into Germany. Attempts to export towel rails to Australia and New Zealand revealed challenges due to these countries' adherence to international safety standards heavily influenced by the EU's CE mark. This experience contradicts one anticipated Brexit advantage: the freedom for UK regulators to diverge from EU safety regulations and adopt a more innovation-friendly approach.

Eskimo’s situation exemplifies a wider trend reflected in trade data. The UK Trade Policy Observatory at Sussex University reported a 26% reduction in the variety of UK exports by 2023. Aston University Business School’s study, analyzing five years of detailed trade data, found a 53.8% decline in export varieties and a 31.5% reduction in import varieties. These "trade varieties" represent the number of different products exported to various EU countries.

A decade ago, many economists predicted long-term economic harm from Brexit, a view now widely supported by data. However, assessing Brexit’s true impact requires comparing actual outcomes with hypothetical scenarios absent Brexit, a process involving complex methodology and statistical judgment. This assessment must also consider major global disruptions since Brexit, including the 2020 pandemic, the 2022 Ukraine conflict, and recent energy price shocks linked to tensions in Iran.

Moreover, it is uncertain whether the UK would have matched the Silicon Valley tech boom’s growth had it remained in the EU. Economists generally agree their analyses account for these global factors, though some critics question their methodologies and the magnitude of Brexit’s effects.

Initial dire predictions from 2016, such as a Great Depression-scale downturn, proved overly pessimistic. While the economic impact was not immediate or severe enough to trigger a recession, many economists assert the UK has nonetheless suffered substantial long-term damage.

"Among economists there is not much debate, but there still is among policy folks. The experts were right. It was, if anything, worse than we thought, but it's taken longer to get there," says Nick Bloom, British Stanford University professor and author of a major recent study using Bank of England data.

Bloom’s research is among numerous academic papers analyzing extensive data to evaluate Brexit’s economic consequences.

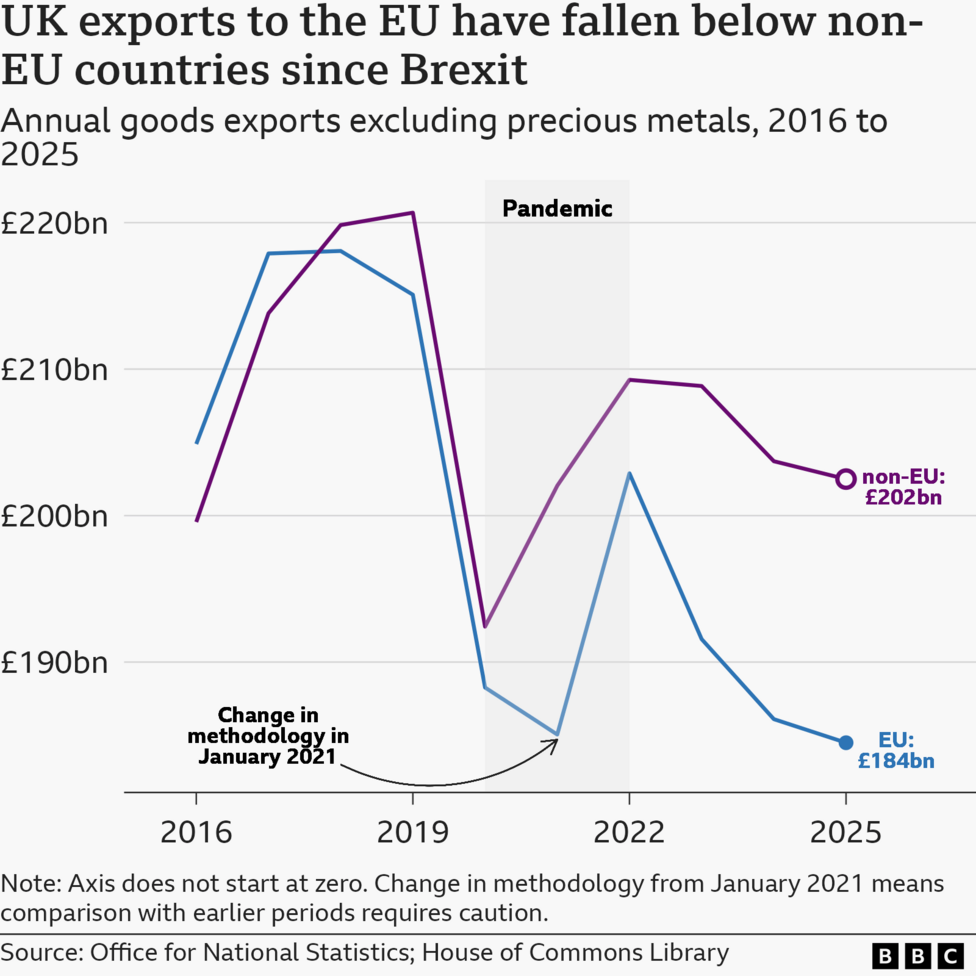

UK trade with Europe

Before 2016, UK trade with Europe was on an upward trajectory. However, official statistics indicate that by 2025, UK exports to the EU had declined by 14% and imports by 10% compared to 2019. The trend worsened, with 2025 marking the worst year for UK goods export volumes to the EU this century, aside from a year during the financial crisis.

The think tank Niesr estimates exports were 16.9% lower and imports 16.1% less than expected based on positive pre-2016 trends. The Centre for European Reform, using a different approach accounting for the UK’s exclusion from recent intra-EU trade growth, estimates a 16% reduction in exports and 14% in imports. Similar declines have been observed in EU countries’ trade with the UK. These figures depend on methodological choices and statistical judgment.

Most studies converge on similar conclusions. However, raw trade figures, unadjusted for inflation spikes, show a 4% increase in UK goods exports to the EU since 2019, a fact some analysts cite to argue Brexit’s impact has been minimal.

Services trade boom

The UK’s services sector, comprising over 80% of economic output, has performed strongly since 2016. UK services exports to the EU rose 57% over the decade, driven by accountancy, legal services, and consultancy. Non-EU services exports increased by 49%. Imports from the EU grew 35%, and imports from outside the EU increased 60%.

While the advanced world has experienced a general services boom, some argue the UK might have performed even better without Brexit. Nonetheless, financial services have fared better than the most pessimistic forecasts made during the referendum campaign.

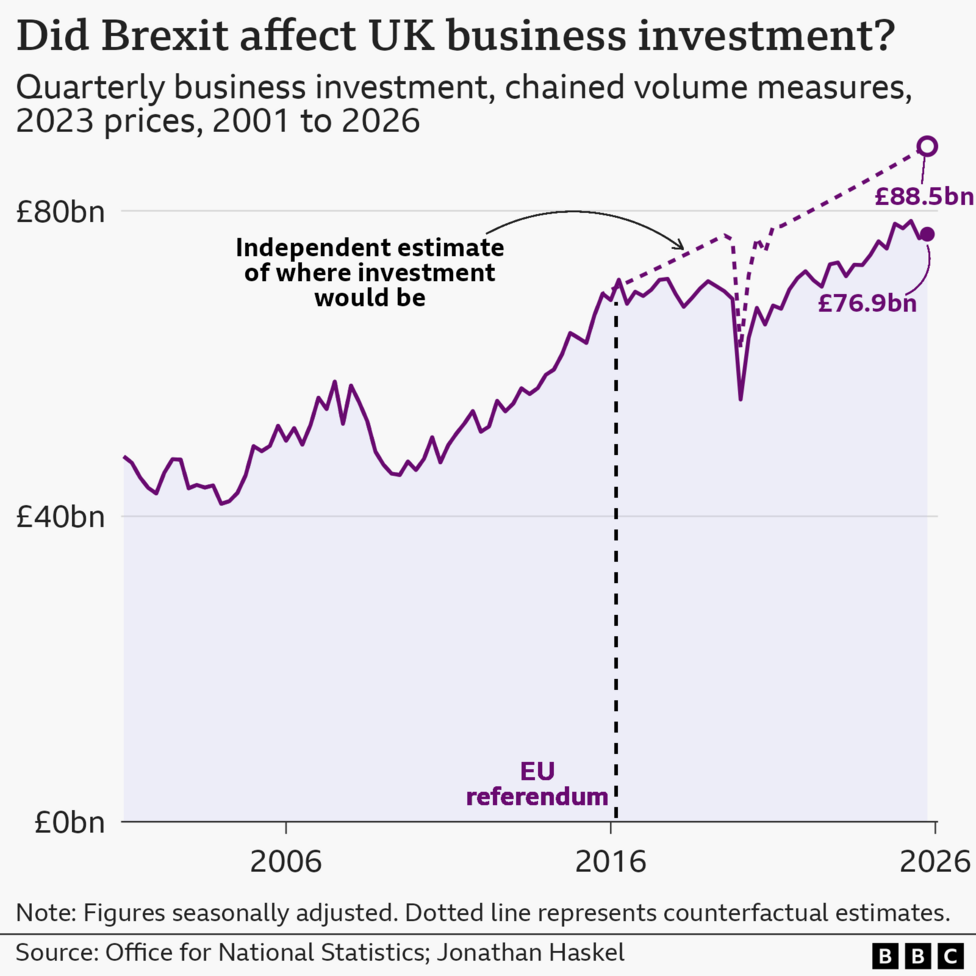

Business investment

Business investment has lagged behind expectations post-Brexit. Jonathan Haskel, former Bank of England economist, estimates a £29 billion (1.3%) reduction in economic size due to lower investment since 2016. Real business investment flattened immediately after the referendum and underperformed long-term UK trends and international comparisons. Haskel calculates a 13% shortfall relative to the 1997-2016 trend.

Other analyses by the National Institute of Economic and Social Research and the US National Bureau of Economic Research (NBER) find UK business investment down 12-13% compared to a basket of advanced economies. These findings mostly predate the 2022 energy crisis and attribute the decline to post-referendum uncertainty. Recent data show the UK trailing most G7 countries but surpassing Germany after its energy shock.

The currency

The pound’s value visibly declined immediately after the referendum and in subsequent years. This depreciation increased costs for imports and travel and reduced the international value of UK assets. Before the referendum, the pound had reached highs against major currencies but fell sharply afterward, particularly against the dollar and euro. Additional declines occurred during Brexit-related uncertainties and the 2022 mini-budget under Prime Minister Liz Truss. Since then, sterling has strengthened, aided by a weaker dollar, and currently sits near its post-Brexit peak.

A weaker pound has raised prices for imported goods, including fresh food and manufactured items, but has also made UK exports more competitively priced internationally. Some food prices have benefited from reduced tariffs on non-UK imports.

The new trade deals

One anticipated Brexit advantage was the UK’s ability to negotiate independent trade agreements. The UK-India deal is highlighted as a significant achievement beyond what might have been possible within the EU. The UK also secured a deal to mitigate President Trump’s tariffs. However, government estimates suggest these deals will only marginally increase economic growth over decades.

Former Prime Minister Tony Blair, a Remain supporter and advocate for a second referendum, recently acknowledged benefits from the UK’s independent AI regulations, noting implications for any future EU re-entry.

Conversely, the EU has signed the Mercosur agreement, granting EU car exporters tariff-free access to Brazil, the world’s sixth-largest market, while UK exporters face a 35% tariff. Although the UK’s deal to alleviate Trump-era tariffs offers a 10% rate compared to the EU’s 15%, the EU benefits from no quota restrictions on car exports to the US, whereas the UK faces a quota of 100,000 units.

Competition between London and Brussels may have accelerated trade dealmaking that otherwise would have taken longer.

The overall hit

The Channel Tunnel, a vital conduit for UK-EU trade, exemplifies Brexit’s impact. In 2016, 1.64 million trucks passed through; by 2025, this fell to 1.16 million, a loss of nearly 30% of high-value cross-Channel freight.

While it is impossible to isolate Brexit’s exact effect from other factors like the pandemic, industry sources describe the decline as "pure Brexit," citing small exporters exiting due to increased costs and shifting business models from "just in time" to stockpiling. HMRC data analyzed by the London School of Economics indicates 16,400 firms (14% of EU exporters) ceased exporting to the EU between 2019 and 2023, predominantly smaller companies.

This decline aligns with academic consensus that the UK economy is smaller than it would have been had Brexit not occurred, with estimates ranging from a 3% to 8% reduction. Nick Bloom attributes about half the loss to increased trade friction with the EU and the other half to political uncertainty during Brexit negotiations.

"The fact that it is harder to trade with the EU is about half the hit, in line with previous forecasts," says Bloom. "The other half is the uncertainty from the fact the Brexit process itself was such an enormous mess… We can never get that second 4% back."

These estimates model a UK economy affected by the pandemic and energy shocks but absent Brexit. The latest NBER study, accounting for population growth, estimates a 6-8% loss in per capita output.

Bloom’s methodologies include considerations of geographic distance, economic gravity, and selective data exclusion. Additional analyses using a Bank of England survey of thousands of firms, representing 10% of private employment, corroborate a roughly 6% smaller economy due to Brexit, equating to an annual growth reduction of approximately two-thirds of a percentage point over the past decade.

Next ten years of Brexit

The global context has transformed dramatically since 2016. Expectations of a US-UK free trade deal contrast with a US now imposing higher trade barriers and weaponizing tariffs. Predictions of EU collapse have not materialized; instead, the EU has strengthened protections for manufacturers. China’s increasing assertiveness further complicates the landscape.

These shifts raise new questions about the UK’s global economic strategy, distinct from those considered a decade ago. An economically independent UK may be well-positioned to navigate volatility, or conversely, UK exporters might benefit from rejoining the EU single market.

Data indicate many UK goods exporters, particularly smaller firms, have not adapted to Brexit, with some sectors showing no improvement.

Policy challenges include aligning with the US’s lightly regulated tech and AI focus while maintaining UK-EU relations. The EU’s "Made in Europe" legislation, requiring a percentage of parts to be produced in Europe, may or may not include the UK. Upcoming tests include steel regulations and a potential UK-EU deal to avoid tariffs on electricity and cars.

UK officials have proposed creating a single market for goods trade with the EU as part of a Brexit reset, though the EU views this as incompatible with UK government red lines on freedom of movement. Unions have shifted from advocating customs union re-entry to seeking a Swiss-style European Economic Area arrangement.

Recently, government ministers have suggested these red lines apply only to the current Parliament and may be reconsidered. The approach of the next prime minister remains uncertain.

The upcoming UK-EU summit has been postponed. Opposition parties have pledged to reverse aspects of the government’s EU reset and post-Brexit deal.

In summary, the status quo is unsustainable. Ten years after the referendum, Brexit and its economic consequences continue to influence the UK, with policy debates poised to intensify.

More from InDepth

- Why the economics make this the craziest World Cup ever

- SpaceX's stock market blast-off could be Musk's biggest gamble yet

- The furious dispute over what caused Air India flight 171 to crash

BBC InDepth offers in-depth analysis and fresh perspectives on major issues, with Emma Barnett and John Simpson curating thought-provoking content weekly. to the newsletter for updates.

Get in touch

Are you personally affected by the issues raised in this story?